Reopen the currency futures market

May 12, 2026

Closing down the market signals unnecessary nervousness and, worse, limits access for smaller players, something RBI has been keen to promote

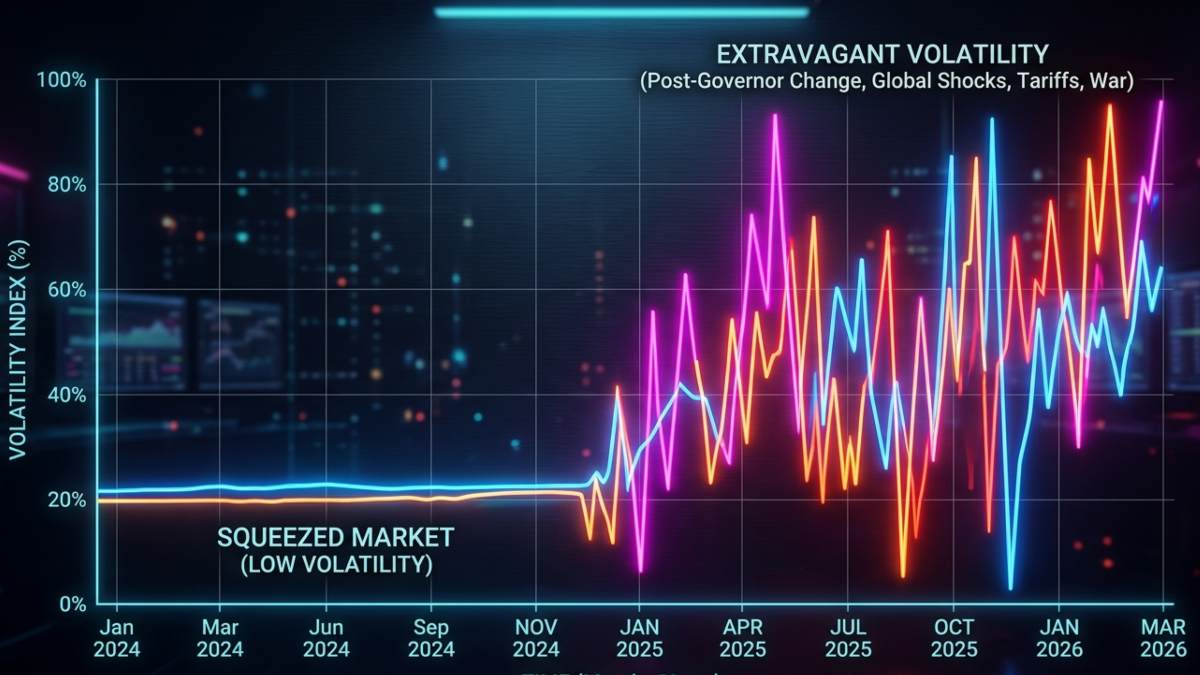

In April 2024, he also executed a near-death squeeze on the currency futures (CF) market, no doubt concerned that it may have been contributing to the difficult volatility the market had faced—volumes fell 90% from $4.1 billion. In my view, this was ill-advised—even at its peak in 2022, the CF market traded less than 5% of the total global rupee volumes, indicating that the impact of CF trading on overall rupee volatility was minuscule.

When Sanjay Malhotra came in as governor (December 2024), probably recognising that near-zero volatility is not conducive to a growing economy with global ambitions, he started allowing more volatility into the market; intra-day volatility also started increasing sharply. Average volatility rose rapidly to about four times its earlier level (although still below the last 10-year average), and the market was getting much healthier.

ALSO READ

But then, Donald Trump’s tariffs and the West Asia war delivered a multi-faceted blow to every country. India was badly affected, more so than most other countries, and the FX market really took it on the chin.

It is well-known that India is extremely vulnerable to rising oil prices, but it also became clear that the Indian economy we had been blindly celebrating was rather like an emperor with very few clothes. Global portfolio investors, who had already recognised this, had been exiting for a couple of years. The expected increase in the current account deficit as a result of the West Asia war increased the pressure and the rupee took an extremely painful tumble, with volatility surging excruciatingly higher.

The severely constrained CF market, of course, remained flat on the ground. In 2025, futures volumes represented only 0.4% of the total global USD/INR volumes, with the big bad non-deliverable forwards (NDF) capturing 58% of rupee volumes. Over the past few months, the Reserve Bank of India (RBI) has had to struggle valiantly to contain the NDF market and, to its credit, has had some limited amount of success.

But it is important to recognise that the NDF market is actually very important to the RBI as part of its effort to internationalise the rupee; Deputy Governor T Rabi Sankar articulated as much when he said that internationalising the rupee is a policy imperative. There has been considerable focus on developing GIFT City as an international hub, and, I believe, many of the teething troubles have been resolved. There are also ongoing efforts at promoting UPI in different countries, and, of course, there are regular negotiations with close partners for rupee invoicing. To be sure, we have some ways to go down that road, partly, of course, because we are not fully convertible on the capital account.

On the other hand, despite the yuan not being fully convertible, China is internationalising quite rapidly. There were recent reports in the Financial Times about a sharp increase in off-shore renminbi borrowing by global banks; this is because Chinese interest rates are extremely low onshore. In Hong Kong, the rates are much lower than USD borrowing costs, even after hedging. To support this, the Chinese government has been encouraging onshore (Chinese) companies to invest in offshore renminbi bonds to create liquidity in that market. But China, and what we can learn from it—and how—is another story.

Coming back to the pavilion, I see no reason for the RBI to continue with the curbs on the CF market. Judging from market volumes, it can only have had marginal (if any) impact on the kind of volatility we have been struggling with. Closing down the market signals unnecessary nervousness and, worse, limits access for smaller players, something that the RBI has quite reasonably been keen to promote.

It launched FX Retail back in 2019 (another creative initiative of Rabi Sankar), but volumes haven’t really taken off. To my mind, this is largely because banks prefer to maintain the non-transparent processes that enables them to squeeze larger margins from small players. It was heartening to hear Governor Malhotra exhorting banks to promote FX Retail more aggressively to their clients. However, his exhortation would have more teeth if the RBI were to, say, monitor the percentage of each bank’s MSME clients who were using FX Retail every quarter or so.

It’s a free country (kind of) and the FX market should be for everybody, not just large players.

When Sanjay Malhotra came in as governor (December 2024), probably recognising that near-zero volatility is not conducive to a growing economy with global ambitions, he started allowing more volatility into the market; intra-day volatility also started increasing sharply. Average volatility rose rapidly to about four times its earlier level (although still below the last 10-year average), and the market was getting much healthier.

ALSO READ

But then, Donald Trump’s tariffs and the West Asia war delivered a multi-faceted blow to every country. India was badly affected, more so than most other countries, and the FX market really took it on the chin.

It is well-known that India is extremely vulnerable to rising oil prices, but it also became clear that the Indian economy we had been blindly celebrating was rather like an emperor with very few clothes. Global portfolio investors, who had already recognised this, had been exiting for a couple of years. The expected increase in the current account deficit as a result of the West Asia war increased the pressure and the rupee took an extremely painful tumble, with volatility surging excruciatingly higher.

The severely constrained CF market, of course, remained flat on the ground. In 2025, futures volumes represented only 0.4% of the total global USD/INR volumes, with the big bad non-deliverable forwards (NDF) capturing 58% of rupee volumes. Over the past few months, the Reserve Bank of India (RBI) has had to struggle valiantly to contain the NDF market and, to its credit, has had some limited amount of success.

But it is important to recognise that the NDF market is actually very important to the RBI as part of its effort to internationalise the rupee; Deputy Governor T Rabi Sankar articulated as much when he said that internationalising the rupee is a policy imperative. There has been considerable focus on developing GIFT City as an international hub, and, I believe, many of the teething troubles have been resolved. There are also ongoing efforts at promoting UPI in different countries, and, of course, there are regular negotiations with close partners for rupee invoicing. To be sure, we have some ways to go down that road, partly, of course, because we are not fully convertible on the capital account.

On the other hand, despite the yuan not being fully convertible, China is internationalising quite rapidly. There were recent reports in the Financial Times about a sharp increase in off-shore renminbi borrowing by global banks; this is because Chinese interest rates are extremely low onshore. In Hong Kong, the rates are much lower than USD borrowing costs, even after hedging. To support this, the Chinese government has been encouraging onshore (Chinese) companies to invest in offshore renminbi bonds to create liquidity in that market. But China, and what we can learn from it—and how—is another story.

Coming back to the pavilion, I see no reason for the RBI to continue with the curbs on the CF market. Judging from market volumes, it can only have had marginal (if any) impact on the kind of volatility we have been struggling with. Closing down the market signals unnecessary nervousness and, worse, limits access for smaller players, something that the RBI has quite reasonably been keen to promote.

It launched FX Retail back in 2019 (another creative initiative of Rabi Sankar), but volumes haven’t really taken off. To my mind, this is largely because banks prefer to maintain the non-transparent processes that enables them to squeeze larger margins from small players. It was heartening to hear Governor Malhotra exhorting banks to promote FX Retail more aggressively to their clients. However, his exhortation would have more teeth if the RBI were to, say, monitor the percentage of each bank’s MSME clients who were using FX Retail every quarter or so.

It’s a free country (kind of) and the FX market should be for everybody, not just large players.