RBI reviews expected credit loss rules amid concerns over impact on SME credit costs

June 01, 2026

The Reserve Bank of India is taking a closer look at its credit loss regulations, which may result in higher borrowing costs for small and mid-sized firms. With rating agencies recently exceeding default rate benchmarks, there is a chance of elevated risk weights for these businesses.

Synopsis

The Reserve Bank of India is taking a closer look at its credit loss regulations, which may result in higher borrowing costs for small and mid-sized firms. With rating agencies recently exceeding default rate benchmarks, there is a chance of elevated risk weights for these businesses.

Mumbai: The Reserve Bank of India is considering a proposal to tweak expected credit loss (ECL) framework amid concerns the rules could weigh on small- and mid-sized companies already facing pressure from the West Asia crisis.

While the framework is aimed at improving rating discipline, it could have unintended consequences, including higher borrowing costs, particularly for smaller firms.

Also Read: India bonds slip ahead of RBI policy as war risks lift oil

The ECL guideline sets strict default thresholds across rating categories, which are linked to banks' capital requirements. If a rating agency breaches these thresholds, lenders must assign higher risk weights to all borrowers in that category, increasing borrowing costs even though the ratings themselves remain unchanged.

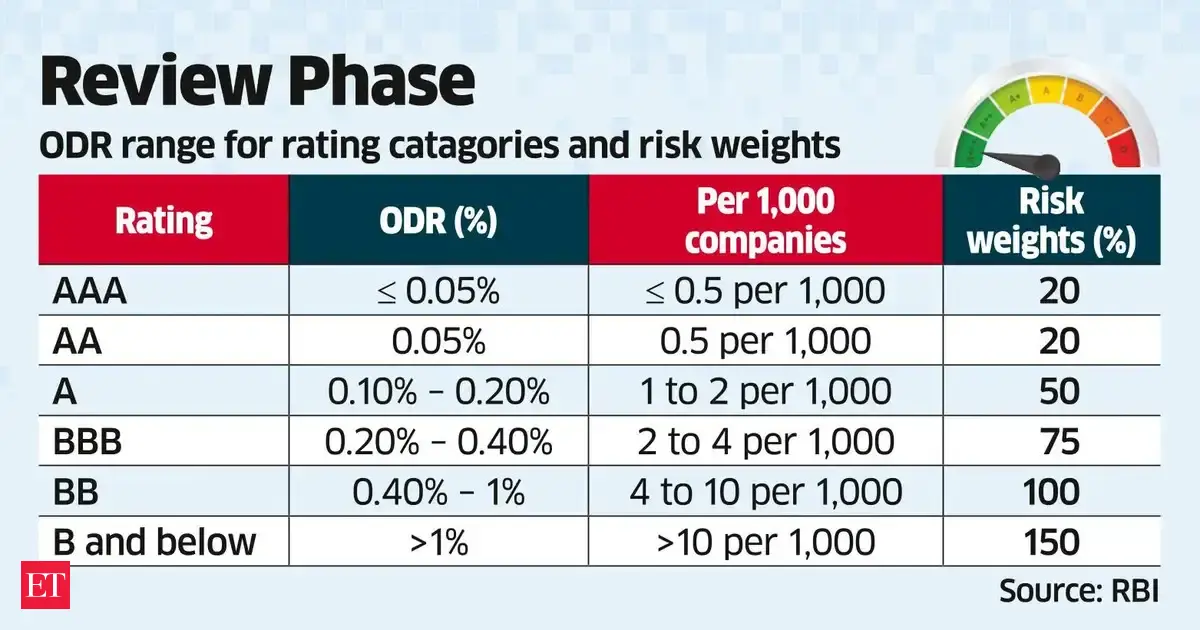

To align risk weights with rating performance, the RBI has introduced an observed default rate (ODR) criterion, which tracks historical defaults within each rating category. If a rating agency's default rate exceeds the prescribed benchmark, banks must apply higher risk weights corresponding to a notch lower rating grade for all companies in that category.

Live Events

For example, the ODR benchmark for BB-rated companies is 0.40-1%, while for BBB-rated firms it is 0.20-0.40%. Most small- and mid-sized firms fall into these two categories.

An analysis of rating data shows all seven rating agencies have breached the ODR in the BB category, implying that risk weights for small and medium-sized firms could rise despite no change in their individual credit profiles.

Bankers said that while the ECL framework had initially reduced risk weights for BB-rated loans to 100%, these benefits may not accrue to borrowers in that category due to breaches in ODR thresholds. Instead, banks will have to assign a 150% risk weight to all BB-rated borrowers. Lenders typically pass on the higher capital costs to borrowers.

The issue was discussed with the RBI at a recent meeting. The RBI did not respond to ET's queries while senior officials at rating agencies declined to comment on the record.

The framework requires agencies to use a four-year historical dataset from April 2023 to March 2027, a period marked by disruptions linked to global conflicts and supply chain shocks.

At the meeting, rating agencies urged the RBI to consider a more prospective approach, arguing that reliance on backward-looking data could distort risk assessments.

Industry participants said the framework, in its current form, could prompt borrowers to shift to larger agencies, reinforcing market dominance by established players and weakening competition. Agencies have also flagged inconsistencies between RBI and market regulator SEBI's benchmarks, which could lead to differing treatment of the same borrower across loans and bonds.

(You can now subscribe to our Economic Times WhatsApp channel)

(Catch all the Business News, Breaking News and Latest News Updates on The Economic Times.)

Subscribe to The Economic Times Prime and read the ET ePaper online.

...moreless

(You can now subscribe to our Economic Times WhatsApp channel)

(Catch all the Business News, Breaking News and Latest News Updates on The Economic Times.)

Subscribe to The Economic Times Prime and read the ET ePaper online.

...moreless

The Reserve Bank of India is taking a closer look at its credit loss regulations, which may result in higher borrowing costs for small and mid-sized firms. With rating agencies recently exceeding default rate benchmarks, there is a chance of elevated risk weights for these businesses.

Mumbai: The Reserve Bank of India is considering a proposal to tweak expected credit loss (ECL) framework amid concerns the rules could weigh on small- and mid-sized companies already facing pressure from the West Asia crisis.

While the framework is aimed at improving rating discipline, it could have unintended consequences, including higher borrowing costs, particularly for smaller firms.

Also Read: India bonds slip ahead of RBI policy as war risks lift oil

The ECL guideline sets strict default thresholds across rating categories, which are linked to banks' capital requirements. If a rating agency breaches these thresholds, lenders must assign higher risk weights to all borrowers in that category, increasing borrowing costs even though the ratings themselves remain unchanged.

To align risk weights with rating performance, the RBI has introduced an observed default rate (ODR) criterion, which tracks historical defaults within each rating category. If a rating agency's default rate exceeds the prescribed benchmark, banks must apply higher risk weights corresponding to a notch lower rating grade for all companies in that category.

Live Events

For example, the ODR benchmark for BB-rated companies is 0.40-1%, while for BBB-rated firms it is 0.20-0.40%. Most small- and mid-sized firms fall into these two categories.

An analysis of rating data shows all seven rating agencies have breached the ODR in the BB category, implying that risk weights for small and medium-sized firms could rise despite no change in their individual credit profiles.

Bankers said that while the ECL framework had initially reduced risk weights for BB-rated loans to 100%, these benefits may not accrue to borrowers in that category due to breaches in ODR thresholds. Instead, banks will have to assign a 150% risk weight to all BB-rated borrowers. Lenders typically pass on the higher capital costs to borrowers.

The issue was discussed with the RBI at a recent meeting. The RBI did not respond to ET's queries while senior officials at rating agencies declined to comment on the record.

The framework requires agencies to use a four-year historical dataset from April 2023 to March 2027, a period marked by disruptions linked to global conflicts and supply chain shocks.

At the meeting, rating agencies urged the RBI to consider a more prospective approach, arguing that reliance on backward-looking data could distort risk assessments.

Industry participants said the framework, in its current form, could prompt borrowers to shift to larger agencies, reinforcing market dominance by established players and weakening competition. Agencies have also flagged inconsistencies between RBI and market regulator SEBI's benchmarks, which could lead to differing treatment of the same borrower across loans and bonds.

(You can now subscribe to our Economic Times WhatsApp channel)

(Catch all the Business News, Breaking News and Latest News Updates on The Economic Times.)

Subscribe to The Economic Times Prime and read the ET ePaper online.

...moreless

(You can now subscribe to our Economic Times WhatsApp channel)

(Catch all the Business News, Breaking News and Latest News Updates on The Economic Times.)

Subscribe to The Economic Times Prime and read the ET ePaper online.

...moreless